US: S&P 500 Index +0.0%, Dow -0.9%, Nasdaq +1.3%

Europe: STOXX Europe 600 +1.0%, German DAX +1.9%, France CAC 40 +1.0%, U.K. FTSE 100 +1.1%

Asia: Japan Nikkei +0.7%, China Shanghai Composite -1.5%, Korea KOSPI -1.9%

Global/Regional: MSCI ACWI +0.1% MSCI EM -0.9% MSCI EAFE+0.2%

Rates/Commodities: 10-Year Treasury yield -2 basis points to 2.92%, WTI crude oil -1.6%, COMEX gold -1.4%

Major U.S. indexes went their separate ways this week as the S&P 500 Index (flat), Nasdaq (rose), and Dow (fell) all reacted differently to a plethora of headline-generating events. This included central bank meetings in the U.S., Eurozone, and Japan, the historic U.S.—North Korea summit, the approval of a high-profile merger in the telecommunications and cable industry, and better-than-expected May retail sales among other economic data. The monetary policy meetings held by the Federal Reserve (Fed) and European Central Bank (ECB) received the most attention, and rightfully so. The Fed’s rate hike announcement was a foregone conclusion, though comments in Chairman Jerome Powell’s post-meeting press conference and the Fed’s outlook for economy provided more interesting insights, as we outlined in our post-meeting blog.

Overseas, developed markets finished near flat, while the MSCI Emerging Markets Index tumbled more than 2% as trade fears and higher U.S. interest rates, which could lead to more dollar strength, helped dampen investor enthusiasm for the group. In Europe, the ECB announced it would end its bond purchases (so-called quantitative easing) by year-end as expected; however, ECB Chief Mario Draghi pledged not to raise interest rates until at least summer 2019. “The balanced approach suggests the ECB has some level of conviction in its economic outlook,” noted LPL Research Chief Investment Strategist John Lynch, “but we continue to favor U.S. and emerging markets equities over the next six-to-twelve months,” a topic we covered in a recent Weekly Market Commentary. With the exception of Japan’s Nikkei, most Asian markets fell progressively throughout the week; trade tensions re-escalated Friday as the U.S. introduced tariffs on Chinese goods worth about $50 billion, to which China immediately retaliated.

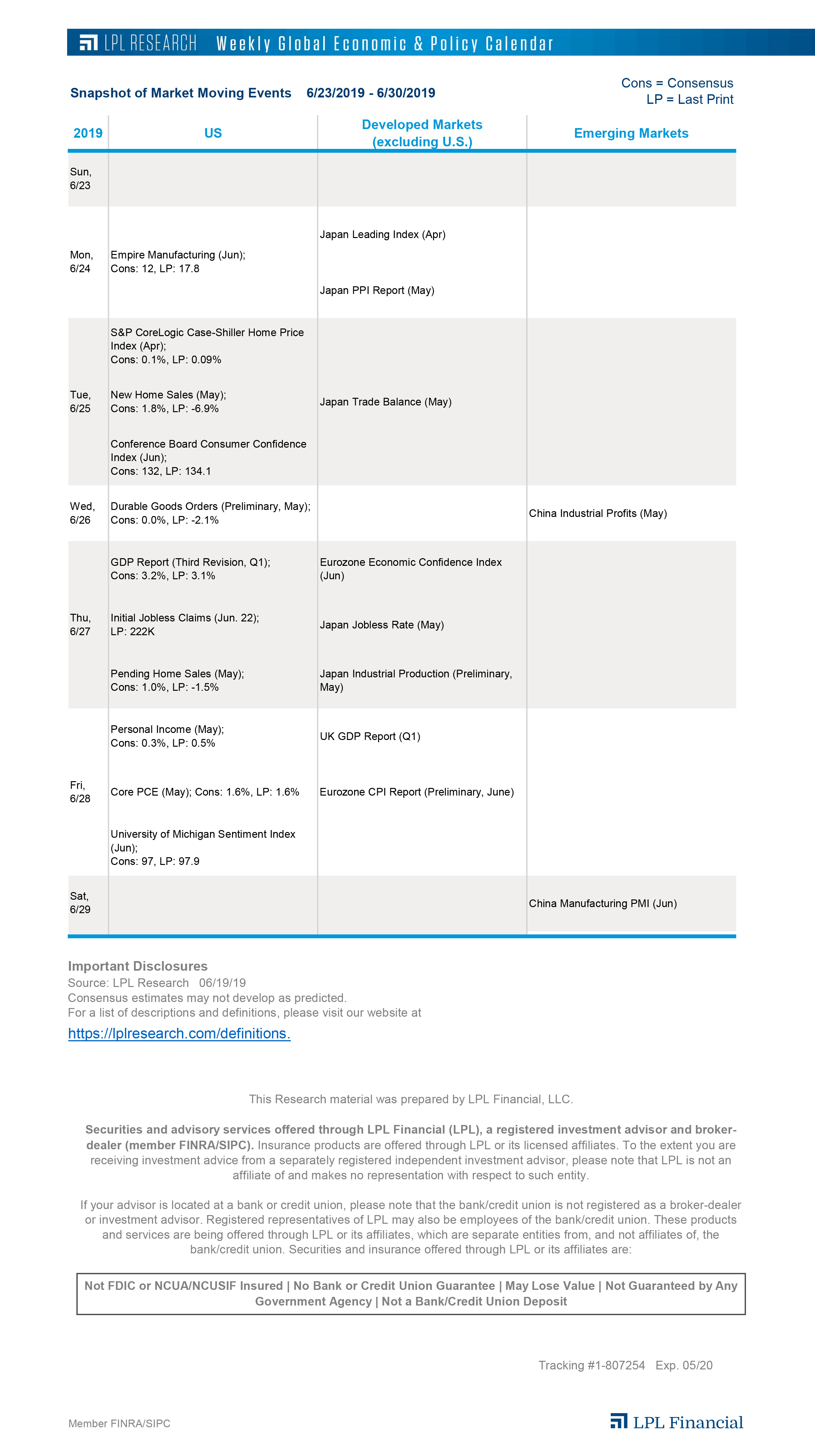

Next week, the housing market will be in focus on the domestic front, while Markit Purchasing Managers’ Index data headlines the economic data releases overseas with figures for France, Germany, the Eurozone, and Japan due out. Get the details in our Weekly Economic Calendar.

{kind=link}

Please see the methodology and assumptions used in GWP.

IMPORTANT: The projections or other information generated by GWP regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. Results may vary with each use and over time.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

Indices are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

Past performance is not indicative of future results. The tax loss harvesting and other tax strategies discussed should not be interpreted as tax advice and there is no representation that such strategies will result in any particular tax consequence. Clients should consult with their personal tax advisors regarding the tax consequences of investing.

Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for any individual security.

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Securities and Advisory services offered through LPL Financial LLC, a Registered Investment Advisor Member FINRA/SIPC

For Client Use – Tracking #1-741040 (Exp. 6/19)